After years in the doghouse for many investors, AT&T ( T ) is firing on all cylinders and returning to its winning ways. I Previously featured AT&T As a contrarian bet in early 2024, when the stock was trading at $17.31, and The stock has performed well since then, gaining more than 35%. I am bullish on the telecom giant based on its more focused and streamlined approach to the business, its commitment to returning capital to shareholders, its attractive 4.9% dividend yield, and its undemanding valuation.

For years, AT&T was known as a dividend stalwart, and many investors relied on Dividend Aristocrat for reliable dividend income every quarter. AT&T hurt its reputation with many of these investors when it cut its dividend in 2022 amid its spinoff to Warner Bros.ers, which merged with Discovery to become Warner Bros. Discovery (WBD). However, the move to spin off Warner Bros. looks like the right decision in retrospect, as the stock has weakened amid a series of struggles.

Meanwhile, AT&T is quietly getting back into the good graces Dividend investors. Stock An attractive 4.9% yieldAbove market averages and above Treasury bonds at a time when interest rates are expected to continue to decline. Also, after the 2022 cut, AT&T’s dividend looks safe and secure, with a dividend coverage ratio of just under 50%. This week, AT&T outlined its multi-year strategic vision at its analyst and investor day, laying out plans to return $40 billion to shareholders over the next three years.

This will be done through a combination of dividend payments and $20 billion 20 billion dollar share buyback. It includes an initial share buyback right to buy back $10 billion worth of shares before the end of 2026. Share buybacks are acceptable to investors because they reduce the number of shares outstanding (thus increasing earnings per share) and can be a sign that management views the shares as undervalued. Buybacks can be especially effective for stocks that pay a large dividend because each share bought back is one share they no longer have to pay a dividend.

AT&T’s Investor Day reaffirmed the fact that AT&T is prioritizing returns to shareholders, and was also a good reminder that it’s a more streamlined business than it was a few years ago. Moves to enter the entertainment business by buying DirecTV in 2015 and Time Warner in 2018 can only be described as big mistakes.

But the good news is that management has recognized these mistakes and moved on from them by separating Warner Bros. through the aforementioned 2022 spinoff and recently selling its remaining 70% stake in the business to TPG, leaving DirectTV, a The transaction is expected to be completed. 2025. These divestitures of subsidiary businesses helped AT&T reduce debt by $25 billion. They also enable AT&T to focus on its bread and butter. As AT&T said at the time of the DirectTV sale, “This sale allows AT&T to focus on leading wireless. 5G and a fiber connectivity company in the US.”

AT&T says it aims to have 50 million fiber locations by 2029 and complete modernization of its 5G network by 2027. AT&T says that investing in fiber and its 5G network has generated strong returns for the business as it has earned about 10 million extra. Cell service customers from mid-2020, increasing annual mobility services income By $9 billion annually during this period. Meanwhile, it has nearly doubled revenue from fiber subscribers over the past three years.

Shares of AT&T are up nearly 40% over the past year. But the good news for investors is that even after this big run, shares are still very cheap.

In fact, shares trade for just 10.7 times 2025 consensus earnings estimates. This is less than half the value of the wider market; The S&P 500 (SPX) trades for more than 25 times earnings. Such undervalued stocks can be more defensive, an attractive feature at a time when the S&P 500 is trading at all-time highs and above historical values. Moreover, if AT&T continues to operate, this redundant majority leaves plenty of room to move forward.

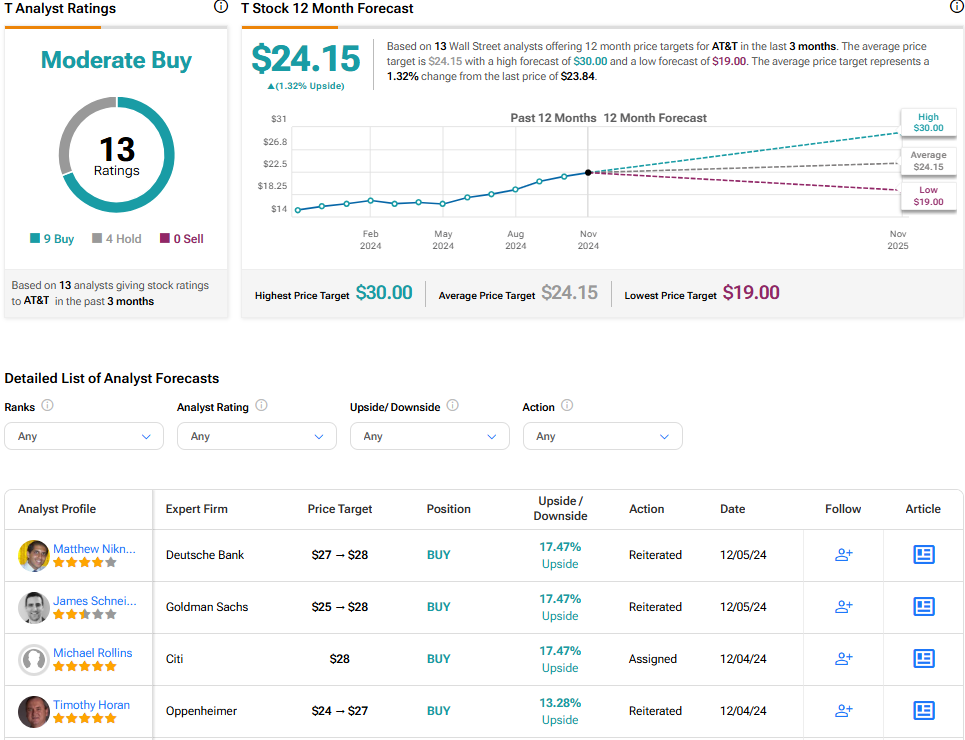

Turning to Wall Street, T earns a moderate buy consensus rating based on nine buy, four hold, and zero sell ratings assigned over the past three months. The Average AT&T stock price target $24.15 implies a 1.3% upside potential from current levels.

I remain bullish on AT&T stock. Even after a strong performance over the past year, the shares still look very cheap, trading at 11 times forward earnings or less than half the market multiple. At a time when the S&P 500 has reached unprecedented heights, it’s not a bad idea for investors to keep some cheap, defensive names in their portfolios.

I’m also bullish on the shares based on an attractive 4.9% dividend yield and management’s intense focus on returning capital to shareholders through a combination of share buybacks and dividend payments of $40 billion over the next three years. While the company has made some mistakes in the past, current management has corrected many of those mistakes, presented a well-defined vision, and is focused on streamlining the business and rewarding shareholders, in my book. makes AT&T a strong buy.