(Bloomberg) — Asian stocks were headed for early declines on Monday after strong U.S. jobs data led traders to reconsider the path forward for a Federal Reserve interest rate cut.

Most read from Bloomberg

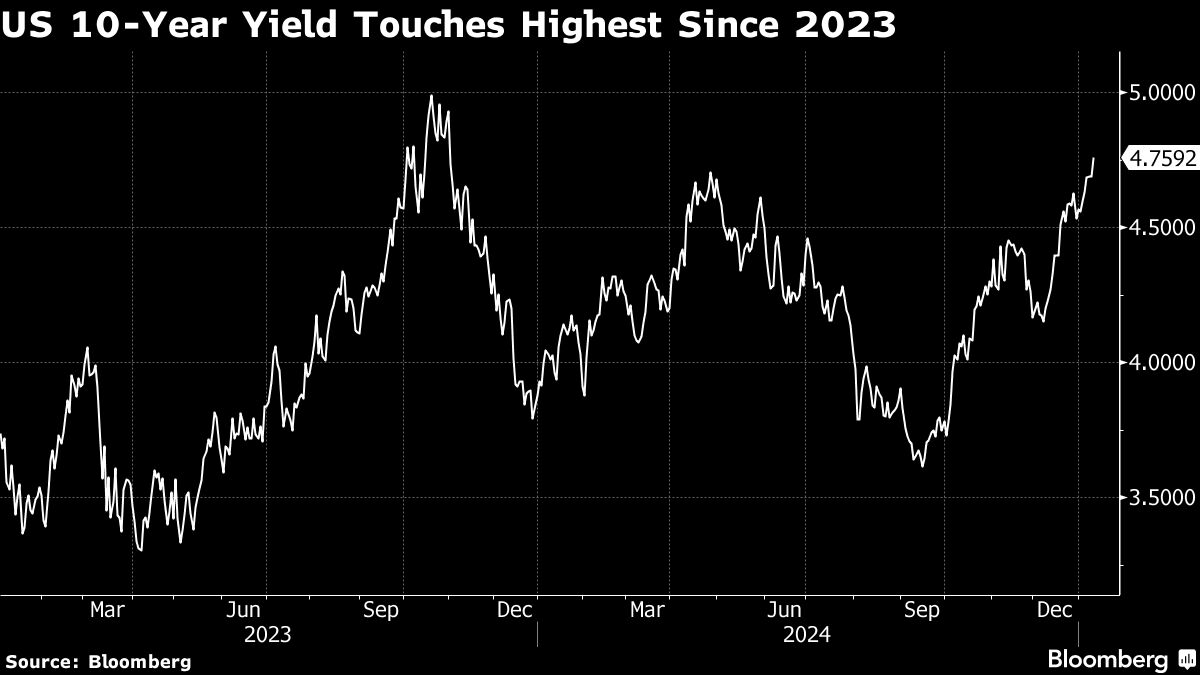

Equity futures for Australia and Hong Kong fell, indicating further pressure on a gauge of the region’s shares that have fallen over the past three sessions. The Japanese market is closed on Monday for a holiday. U.S. stocks and Treasuries fell after Friday’s report, with the S&P 500 down 1.5% and the Nasdaq 100 down 1.6%. The 10-year yield rose seven basis points to close at 4.76%, a level not seen since 2023.

Australian and New Zealand bond yields also climbed early Monday. The dollar traded within narrow ranges after strengthening against most major currencies on Friday, pushing an index of greenback strength to a two-year high. The yen was an outlier, paring a recent decline against the dollar, after Bank of Japan officials indicated they might consider raising their inflation outlook at a policy meeting later in January.

The selloff in stocks and renewed enthusiasm for the dollar reflected the caution that has marked the early weeks of the year as traders remain uncertain about Federal Reserve cuts and the pace of inflation.

Elsewhere, options traders are bracing for the pound to fall as much as 8% as the financial crisis that prompted a painful sell-off weighed on the currency in UK markets last week.

In Asia, data to be released on Monday includes December trade data for China and inflation for India. Separate data on China’s December money supply could also be released anytime until January 15.

Economic data for China will provide investors with further evidence of the challenges facing the world’s second-largest economy. Chinese stocks are facing their worst start to a year since 2016 after falling more than 5% in the first seven trading sessions of 2025.

Strong jobs

With the Consumer Price Index report out on Wednesday, investors will turn their attention to signs of US inflation in data to be released this week. They will also watch the New York Fed’s one-year inflation expectations on Monday, producer prices on Tuesday and jobless claims on Thursday.

The data will provide further clarity on the US economy after Friday’s blow-out nonfarm payrolls data. US employment rose by the most in nine months in December and the unemployment rate fell sharply, capping another year of resilience in the labor market. The data supported the view that US rates could be on hold for the foreseeable future, a possibility suggested by a handful of Fed officials last week.

After Friday’s jobs data, economists at some major banks revised their forecasts for additional Fed rate cuts.

Bank of America Corp., which previously expected two quarter-point cuts this year, now expects none, and said the next move risks an increase. Citigroup Inc. — whose rate-cut outlook is one of Wall Street’s highest expectations — still sees five quarter-point cuts, but says they will start in May. Goldman Sachs Group Inc. This year sees two cuts compared to three.

“Investors may want to brace themselves for more volatility as the market realigns expectations for lower cuts,” said Gina Bolwin at Bolwin Wealth Management Group.

In corporate news, Johnson & Johnson Intra-Cellular Therapies Inc. is exploring a bid to acquire , people familiar with the matter said. Bain Capital has sweetened its bid for Australia’s Insignia Financial Ltd as takeover activity heats up for the wealth manager.

Jamie Dimon of JPMorgan Chase & Co. said tariffs, if used properly, can help address issues such as unfair competition and national security.

Among commodities, oil settled at a three-month high on Friday as the U.S. increased sanctions against Russia, adding to a bullish development pushing crude to a strong start to 2025.

Highlights of this week:

China Business, Monday

India CPI, Monday

ECB Chief Economist Philip Lane and Governing Council Member Olli Rehn, speaking in Hong Kong on Monday

Argentina CPI, Tuesday

US PPI, Tuesday

New York Fed President John Williams speaking on Tuesday

Bank of Japan Deputy Governor Ryozo Himino speaking on Tuesday

Eurozone industrial production, Wednesday

France CPI, Wednesday

UK CPI, Wednesday

US CPI, Wednesday

Chicago Fed President Austin Goolsbee, Minneapolis Fed President Neil Kashkari spoke on Wednesday.

ECB Governing Council member François Villeroy de Galhou speaking, Wednesday

Australia Unemployment, Thursday

Germany CPI, Thursday

Italy Business, CPI, Thursday

Poland rate decision, Thursday

South Korea’s rate decision, Thursday

UK Industrial Production, Thursday

US initial jobless claims, retail sales, import prices, Thursday

Bank of America, Morgan Stanley earnings, Thursday

TSMC Earnings, Thursday

China GDP, property prices, retail sales, industrial production, Friday

Eurozone CPI, Friday

US housing starts, industrial production, Friday

Some key moves in the markets:

Stock

Currencies

The euro was little changed at $1.0241

The Japanese yen was little changed at 157.81 per dollar

The offshore yuan was little changed at 7.3619 per dollar

Cryptocurrency

Bitcoin fell 0.5% to $93,904.01

Ether fell 0.8% to $3,239.84

bond

This story was produced with assistance from Bloomberg Automation.