Finding a compelling growth stock to step into is usually not difficult. Choosing a growth stock that you feel confident holding for a decade or more, however, is a different story. Some storied stocks don’t have enough proven potential for investors to make a long-term commitment to them.

Are you missing the morning scoop? wake up with Breakfast news to your inbox every market day. Sign up for free »

Still, investments that fit that bill do exist. If you can handle the risk, these three stocks have the potential to be amazing winners for investors who buy and hold for at least 10 years.

Investing in Drug companies Can be a complicated business. If you dive in too early, you may learn the hard way that a potential miracle drug in development is actually a bust. If you wait too long, you could miss out on a lot of the stock’s gains.

With this in mind, risk-tolerant investors should take a look Iowans Biotherapeutics(NASDAQ: IOVA ) While shares are still down more than 80% from their early 2021 peak.

Such pullbacks are not particularly uncommon for small names in the biopharma industry. Iovance soared when its flagship drug first started showing promise in clinical trials in 2019 and 2020. However, investors got a little ahead of themselves. The first regulatory approval of its cancer-fighting AmtagV did not materialize until February this year. While the market rewarded the company for that achievement with a jump in share price, by then most of the bullish euphoria had already worn off. And most of the gains the stock booked earlier this year have since evaporated.

But you can use the stock’s current weakness to your advantage.

Although Amtagavi’s FDA-approved uses may currently be relatively narrow — it’s only approved for the treatment of certain types of solid tumors — this T-cell therapy is a potential treatment for a very wide range of cancers. is The drug is currently being tested in 12 other clinical trials, and a handful of them are promising late-stage trials.

But even without any future approvals, Iovance is already doing great work with Amtagvi. Last quarter’s revenue was $58.6 million Marked improvement That was impressively early revenue of $31.1 million in Q2, bringing the company to a full-year top line of nearly $160 million. Sales are expected to rise from $450 million to $475 million next year. However, this is only the beginning. The analyst community is predicting revenues of more than $700 million in 2026, while research organization GlobalData believes AmtagV’s annual sales could eclipse $1 billion by 2030.

However, there are risks for investors to keep in mind. Chief among them is the large amount of money Iovance is still losing despite strong initial demand for its flagship T-cell therapy. While there is nothing unusual about early losses within the biopharma industry, there is no clear picture of when the company will get out of the red and black. Even analysts don’t expect real profits until 2027. A lot can happen between now and then, so you want to carefully consider the size of any position in this stock.

Amtagwi needs time to reach its proverbial cruising speed, so the challenge for investors will be to be patient to allow Iowans to make the most of the opportunity.

As long as there are computers and networks connected to the Internet, criminals will try to exploit them digitally. Indeed, cyber security organizations Check point software reports that weekly cyberattacks rose a record 75% year-over-year during the third quarter, up from Q2’s 30% increase.

This problem is not going away anytime soon, however Palo Alto Networks(NASDAQ: PANW) Ready to answer the call.

Simply put, Palo Alto helps enterprises of all shapes and sizes protect themselves from cybercrime and other types of digital disruption. From threat detection to malware defense to phishing protection to remote employee logins (and more), this company can handle almost any cybersecurity need. And it can do so with easy-to-use turnkey solutions that allow for minimal user interface.

That’s one reason why, in 2024, Palo Alto was once again ranked by the Technology Market Research Organization. Gartner As a leader in the endpoint protection platform market. Additionally, for the eleventh consecutive year, Gartner ranked Palo Alto as a leader in the network firewall market. The company is good at what it does.

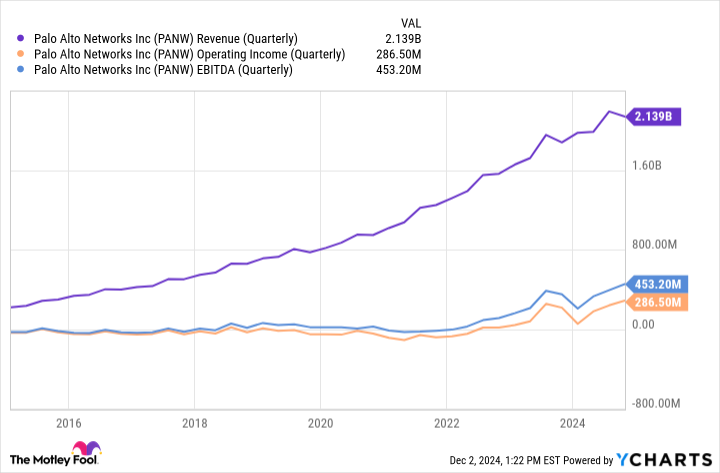

This is also evident from its financial results. Not only has its revenue grown every quarter for more than a decade, but its operating income and EBITDA (earnings before interest, taxes, depreciation, and amortization) have grown almost reliably.

Then, there’s a detail to this progress that isn’t as readily apparent: Palo Alto Networks’ profit margins are also increasing. Whether its software is sold to 100 customers or 1,000, the cost of coding and deploying it is about the same. This is the power of scale. The recurring revenue booked from subscription-based access to its tools doesn’t hurt either.

Palo Alto is positioned to capitalize on growth across the cybersecurity industry as analysts expect the company to deliver 14% top-line growth in its fiscal year 2025 before accelerating to around 16% next year.

Finally, add Wolfspeed(NYSE: WOLF ) On your list of potential monster stocks you might want to hold for the next 10 years.

Unless you’re an electrical engineer, the term “silicon carbide” probably doesn’t mean much to you. That will be in the foreseeable future, though, and Wolfspeed’s time in the spotlight will be as a result.

Layman’s Explanation: Almost all electrical appliances require minimum usage something Silicon-based components. In the past, generic silicon was perfectly fine to meet the technology needs of the times. Things are changing, however. Thanks to dramatic improvements in other technologies, old-fashioned silicon is no longer sufficiently power-efficient, nor capable of efficiently handling the high voltages required by heavy-duty equipment such as electric vehicles or data center power platforms.

Enter Wolfspeed, which has mastered (and patented) the art and science of adding carbon to silicon to make the material more efficient as well as capable of handling higher electrical loads.

Although its potential applications are vast, the most practical use of silicon carbide today is on the heavy machinery and industrial front. Wolfspeed’s technology is increasingly used in electric vehicles as part of their powertrain as well as their charging equipment, resulting in 80% less power loss than currently used battery/reverse/motor combinations. You’ll find its technology in a growing number of construction vehicles, agricultural machinery and even locomotives.

At the other end of the size scale, you’ll find its silicon carbide inside chips and components attached to circuit boards in HVAC equipment and data center power supplies, where its offerings can achieve up to 99% energy efficiency at half the size. are Common silicon.

While the benefits of silicon carbide are clear, not every customer is consistent with Wolfspeed’s products. After growing its revenue by 24% in fiscal 2023 (ended June 2023), growth nearly stalled in fiscal 2024, leading to a pattern of top-line inconsistency that has been frustrating investors for over a decade. Wolfspeed is reporting heavy losses as a result. The analyst community doesn’t see net profits returning until fiscal 2027 when the next generation of EVs hit the roads. And When the company finally puts several restructuring charges and significant capital expenditures in the rearview mirror. All this strategic maneuvering and spending is a big reason why shareholders have experienced a wild roller coaster ride.

If you can stomach the constant volatility, however, this stock is worth it. Analysts expect Wolfspeed to report 44% sales growth in fiscal 2026, which the company itself believes will be enough to generate breakeven operating cash flow. And management believes the company could return to EBITDA profitability during the second half of this year, on track to return to profitability in fiscal 2027.

And for the long term, Global Market Insights believes that the world’s silicon carbide market is expected to grow at a compound annual rate of more than 30% through 2032. But most of this development is set to take place in the latter half of this timeframe when the technology becomes industry-standard.

Owning this high-potential stock means living with above-average near-term risk. Investors will have to focus on how well this silicon carbide leader can navigate the industry’s long-term potential. The market should begin to reward Wolfspeed’s progress toward profitability in the meantime.

Before buying stock in Palo Alto Networks, consider this:

The Motley Fool Stock Advisors The analysis team has just identified what they believe 10 best stocks For investors to buy now… and Palo Alto Networks was not one of them. 10 stocks to make the cut can generate amazing returns in the coming years.

Consider when nvidia This list was created on April 15, 2005… If you invested $1,000 at the time of our recommendation, You will have $872,947!*

Stock advisor Provides investors with an easy-to-follow blueprint for success, including portfolio construction guidance, regular updates from analysts, and two new stock picks every month. TheStock advisorThe service is More than quadruple Return of the S&P 500 since 2002*.

James Brumley No positions in any of the stocks mentioned. The Motley Fool has positions and recommends Iovance Biotherapeutics and Wolfspeed. The Motley Fool recommends Gartner and Palo Alto Networks. Motley Fool has a Disclosure Policy.